The Most Common Investing Mistake to Avoid

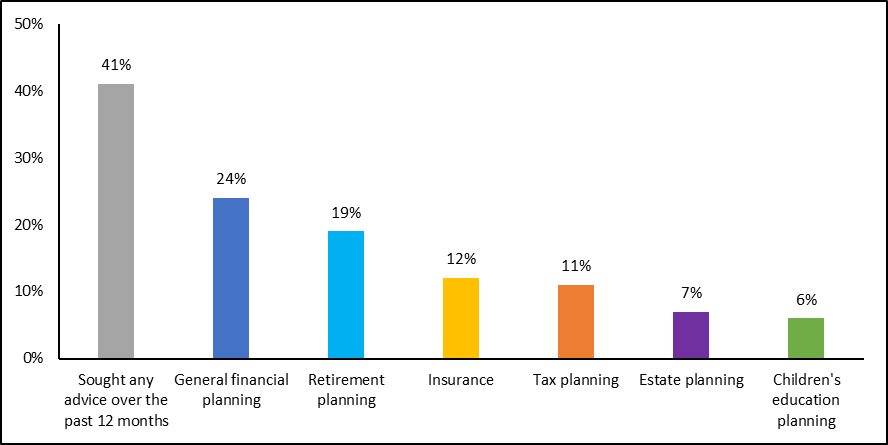

Thinking about investing but don’t want to lose your money? You’re not alone. 80% of Canadians have sought advice about financial planning in the past 12 months.

Investing in the stock market or other asset classes can be both an exciting but nerve-racking experience. As an IIROC certified financial planner, I have years of experience helping my clients make sound investment decisions. That’s why in this article, I will teach you common investing mistakes to avoid.

Table of Contents

ToggleNot Having a Clear Investment Plan or Goals

Not having a clear investment plan or goals is a common investing mistake that can lead to suboptimal financial outcomes. An investment plan serves as a roadmap for your financial journey, helping you make informed decisions that align with your objectives, risk tolerance, and time horizon. Without a well-defined plan, investors may struggle to achieve their financial goals, make poor investment choices, or become easily swayed by market fluctuations.

Here’s why having a clear investment plan and setting goals is important:

- Identifying financial objectives: Defining your financial goals, such as saving for retirement, buying a home, or funding a child’s education, helps you determine the required investment strategies and instruments. Each goal may have a different time horizon and risk tolerance, which can influence your investment approach.

- Assessing risk tolerance: Understanding your risk tolerance enables you to select suitable investments that align with your comfort level. A clear investment plan helps you avoid taking on excessive risk or being overly conservative, both of which can impact your long-term returns.

- Asset allocation: With well-defined goals and risk tolerance, you can determine an appropriate asset allocation, which is the mix of stocks, bonds, and other assets in your portfolio. Asset allocation is a key factor in managing investment risk and achieving your financial objectives.

- Time horizon: Knowing your investment horizon for each goal helps you make appropriate investment choices. For example, a longer time horizon may allow you to take on more risk and invest in higher-return assets, while a shorter time horizon may require a more conservative approach.

- Performance tracking: A clear investment plan helps you monitor your progress towards achieving your financial goals. Regularly reviewing your investments allows you to make adjustments if necessary, such as rebalancing your portfolio or changing your investment strategy.

- Discipline and focus: An investment plan promotes discipline and keeps you focused on your long-term objectives, reducing the likelihood of making impulsive decisions driven by emotions or market fluctuations.

To create a clear investment plan, start by outlining your financial goals, assessing your risk tolerance, and determining your time horizon for each objective. Then, select appropriate investments and asset allocations that align with your plan. Regularly review and adjust your plan as needed to stay on track towards achieving your financial goals. Consider consulting a financial professional for guidance in creating a personalized investment plan.

Failing to Diversify

Failing to diversify is a common investing mistake that can expose your portfolio to unnecessary risks and negatively impact your long-term returns. Diversification is the process of spreading your investments across different asset classes, industries, and geographic regions to minimize the impact of any single investment or market event on your overall portfolio. 21% of Americans think that exposure to the stock market is key to intelligent investing. However, you shouldn’t put all of your eggs in one basket.

Here’s why diversification is important and how it can benefit your investment strategy:

- Risk reduction: By holding a diverse mix of investments, you can reduce the impact of poor performance by a single asset or a specific sector. If one investment underperforms, the other investments in your portfolio can help offset the loss, mitigating the overall risk.

- Smoother returns: Diversification can lead to smoother portfolio returns over time since different assets often perform differently under varying market conditions. This can help protect your portfolio from extreme fluctuations and potentially lead to more consistent returns.

- Exposure to opportunities: Diversifying your investments across industries, asset classes, and regions allows you to participate in the growth of various sectors and markets. This can improve your chances of benefiting from strong performers, which may not be possible if you are heavily concentrated in a single area.

- Long-term performance: Studies have shown that a well-diversified portfolio typically delivers better risk-adjusted returns over the long run than a concentrated portfolio. This means that, for a given level of risk, a diversified portfolio is likely to generate higher returns.

Here are some tips to help you achieve diversification in your investment portfolio:

- Spread investments across asset classes: Allocate your investments among different asset classes, such as stocks, bonds, and cash equivalents, based on your risk tolerance and investment objectives.

- Diversify within asset classes: Within each asset class, invest in a variety of sectors, industries, and company sizes to avoid concentration risk. For example, in your stock allocation, consider investing in companies from different sectors, such as technology, healthcare, financials, and consumer goods.

- Geographic diversification: Invest in both domestic and international markets to benefit from global growth opportunities and reduce the impact of regional economic events.

- Use diversified investment products: Mutual funds, index funds, and exchange-traded funds (ETFs) can offer built-in diversification by investing in a broad array of securities within a single fund.

- Rebalance regularly: Periodically review and adjust your portfolio to maintain your target asset allocation and diversification.

Remember that while diversification helps reduce risk, it does not eliminate it completely. It’s essential to carefully assess your investments, align them with your financial goals and risk tolerance, and consult a financial professional if needed.

Investing Without Understanding

Investing without understanding refers to the practice of putting money into assets, financial instruments, or investment strategies without fully grasping their fundamentals, risks, or potential rewards. This common investing mistake can lead to poor decision-making, increased risk, and disappointing returns. It’s essential to have a thorough understanding of any investment you consider to ensure that it aligns with your financial goals and risk tolerance.

Here’s why investing without understanding is risky and how you can avoid this mistake:

- Inappropriate risk exposure: If you don’t fully comprehend an investment, you may unintentionally expose your portfolio to higher risks than you’re comfortable with, or you may miss out on potential growth opportunities due to an overly conservative approach.

- Unrealistic expectations: Without understanding the potential rewards and risks associated with an investment, you might set unrealistic expectations for returns, leading to disappointment or impulsive decisions driven by emotions.

- Susceptibility to fraud or scams: A lack of understanding can make you vulnerable to investment fraud or scams, where malicious actors take advantage of your limited knowledge to sell you unsuitable or fake investments.

- Inefficient portfolio management: Investing in assets or strategies that you don’t understand can make it challenging to monitor and manage your portfolio effectively, potentially leading to suboptimal performance.

To avoid investing without understanding, consider the following steps:

- Education: Dedicate time to learning about various investment options, financial instruments, and strategies. This may include reading books, attending seminars or webinars, and using online resources to increase your financial knowledge.

- Research: Thoroughly research and analyze potential investments, paying close attention to their fundamentals, historical performance, risks, and fees. Understand how each investment fits into your overall portfolio and contributes to your financial goals.

- Seek professional guidance: If you’re unsure about an investment or lack the necessary knowledge, consider consulting a financial professional, such as a financial advisor or planner, for guidance and advice tailored to your individual circumstances.

- Start with simpler investments: Begin with relatively straightforward investments, such as index funds or blue-chip stocks, before venturing into more complex assets or strategies, like options, futures, or leveraged ETFs.

- Be patient and disciplined: Avoid jumping into investments based on hype, trends, or “hot tips.” Take your time to understand the investment and its suitability for your portfolio before committing your money.

By ensuring that you understand the investments you make, you’ll be better equipped to manage your portfolio effectively, make informed decisions, and work towards achieving your financial goals.

Timing The Market

There is no right or wrong time to invest, as the average person starts investing at the age of 33. Timing the market, however, involves attempting to predict the best times to buy or sell investments based on anticipated future price movements. The goal is to buy low and sell high, thereby maximizing returns. However, timing the market is generally considered a bad idea for most investors for several reasons:

- Difficulty in prediction: Accurately predicting market movements is extremely challenging, even for experienced professionals. Financial markets are influenced by numerous factors, such as economic data, geopolitical events, corporate earnings, and investor sentiment, making it nearly impossible to consistently forecast short-term price fluctuations.

- Increased risk: Attempting to time the market can expose you to higher risk, as you may end up buying or selling assets at inopportune times. For example, selling out of fear during a market downturn may result in locking in losses, while waiting for the “perfect” buying opportunity could lead to missing out on potential gains.

- Higher costs: Active trading that involves frequent buying and selling of assets can lead to increased trading costs, such as commissions and bid-ask spreads. These costs can erode your investment returns over time.

- Emotional decision-making: Market timing often involves making decisions based on emotions, such as fear or greed, rather than following a disciplined investment strategy. Emotional investing can lead to impulsive choices that deviate from your long-term financial goals and result in suboptimal performance.

- Missed compounding opportunities: By attempting to time the market, you may miss out on the benefits of compounding, which refers to the growth of your investments through the reinvestment of earnings. Staying invested over the long term allows your returns to compound, which can significantly contribute to your overall investment growth.

Instead of trying to time the market, most investors are better served by adopting a long-term, disciplined investment strategy that focuses on diversifying their portfolio, regularly contributing to their investments, and periodically rebalancing their asset allocation.

Ignoring Fees and Expenses

Ignoring fees and expenses when investing is a mistake because they can have a significant impact on your returns over time. When you invest, you might come across various fees, such as trading commissions, management fees, account maintenance fees, and expense ratios for mutual funds or ETFs. These costs might seem small, but they can really add up and eat into your profits, especially in the long run.

Think of it this way: if you have two similar investments with slightly different fees, choosing the one with lower fees can save you money and result in higher returns over time. It’s like choosing between two items at a store – if they’re pretty much the same, you’d probably pick the one with the lower price, right?

It’s essential to be aware of the fees associated with your investments and to factor them into your decision-making process. Don’t just focus on the potential gains; consider the costs as well. Compare fees across different investment options, platforms, or advisors, and choose the ones that offer a good balance between cost and performance. This way, you can keep more of your hard-earned money working for you, and your investments will have a better chance of growing over time.

Remember, every dollar you save on fees is a dollar that can be reinvested and compound over time, helping you reach your financial goals more efficiently. So, don’t ignore those fees and expenses – they matter more than you might think!

Emotional Investing

Emotional investing is when you let your feelings, like fear or excitement, guide your investment decisions instead of sticking to a well-thought-out plan. It’s a mistake because it can lead to impulsive choices that might hurt your financial goals in the long run. In fact, 58% of investors agree that leaving emotions out of their decisions results in better portfolio performance.

Imagine you’re at a party, and everyone’s talking about a hot new stock that’s skyrocketing. You might feel the urge to jump in and buy it, too, because you don’t want to miss out on the gains. That’s called “FOMO” or the fear of missing out. On the flip side, if the market takes a downturn, you might panic and sell your investments to avoid losing more money, which is usually driven by fear.

The problem with emotional investing is that it can cause you to buy high and sell low, which is the opposite of what you should be doing. Instead of making decisions based on short-term market fluctuations or what everyone else is doing, it’s better to have a solid investment plan and stick to it. That way, you’ll be less likely to make impulsive choices and more likely to achieve your long-term financial goals.

So, next time you feel the urge to make a move based on emotions, take a step back, and remind yourself of your plan. Maybe even talk to a financial advisor or a trusted friend to get a second opinion. Remember, investing is a marathon, not a sprint, and keeping a cool head can really pay off in the end.

Chasing Past Performance

You know how they say, “hindsight is 20/20”? Well, that’s kind of the problem with chasing past performance. When you see an investment that has done really well in the past, it’s tempting to think, “If I just invest in this now, I’ll make a killing, too!” But the truth is, past performance isn’t a guarantee of future success.

Think of it like a sports team that won the championship last year. Sure, they might be good, but it doesn’t mean they’ll win again this year. There are so many factors that can change – new players, injuries, or even just plain luck.

It’s the same with investments. Companies and markets change, and what worked well in the past might not be the best choice for the future. Plus, by the time you jump on the bandwagon, you might be getting in when the investment is already overvalued, which could lead to lower returns or even losses.

So, instead of chasing past performance, it’s better to focus on the fundamentals of the investment, like the company’s financial health, industry trends, and growth potential. And don’t forget to diversify your portfolio to spread the risk. That way, you’ll be more likely to make informed decisions and achieve your financial goals, rather than just chasing what was hot yesterday.

Overconfidence

You know how sometimes people think they’re better at something than they actually are? That’s overconfidence, and it can be a real problem when it comes to investing. When you’re overconfident, you might think you’ve got everything figured out and can predict the market like a pro. But the truth is, nobody can predict the market perfectly, not even the experts!

Overconfidence can lead to some not-so-great decisions, like putting too much money into a single investment because you’re sure it’s a winner, or trading too frequently because you think you can outsmart the market. And when things don’t go as planned, you might be slow to admit your mistakes or change course.

The thing is, investing is a complex game with a lot of moving parts, and even the best-laid plans can go awry. That’s why it’s important to stay humble, be open to learning, and recognize that there’s always some level of uncertainty.

A good approach is to have a well-thought-out investment plan and stick to it, even when things get tough. And remember, diversification is your friend – by spreading your investments across different assets, industries, and regions, you can help protect your portfolio from unexpected surprises. So, keep your confidence in check, and your investments will be better off for it!

Inadequate Research

Inadequate research is a common investing mistake that can lead to poor investment decisions and financial losses. Thorough research helps investors understand the financial health, future prospects, and risks associated with a particular investment. This insight allows them to make informed decisions, minimize the potential for loss, and seize opportunities for growth. Here, we’ll discuss why inadequate research is a prevalent issue and offer some tips on how to avoid it.

Reasons for Inadequate Research:

- Overconfidence: Some investors may believe they have enough knowledge or intuition to make profitable decisions without conducting proper research.

- Information Overload: The sheer volume of financial data and news available can be overwhelming, leading investors to take shortcuts or rely on overly simplistic analysis.

- Time Constraints: Researching investments thoroughly can be time-consuming, and some investors may not be willing or able to dedicate sufficient time.

- Herd Mentality: Some investors may follow the decisions of others, assuming that the majority opinion must be correct, instead of conducting their research.

How to Avoid Inadequate Research:

- Set Realistic Expectations: Understand that investing requires time and effort. Allocate sufficient time for research and be prepared to learn from mistakes.

- Develop a Research Process: Establish a systematic approach to researching investments, such as fundamental analysis, technical analysis, or a combination of both.

- Diversify Information Sources: Seek information from various sources, including financial statements, industry reports, and news articles, to ensure a comprehensive understanding of the investment.

- Use Reliable Sources: Ensure that the information you collect comes from reputable sources, such as government publications, reputable financial news outlets, and company reports.

- Stay Updated: Keep up with market news, industry developments, and the performance of your investments. Regularly review your investment decisions to ensure they remain aligned with your financial goals.

- Leverage Expertise: If you lack the time or expertise to conduct thorough research, consider seeking professional advice from a financial advisor or using investment tools and platforms that offer in-depth analysis and research resources.

- Keep Emotions in Check: Avoid making investment decisions based on emotions, such as fear or greed. Instead, rely on objective data and thorough research.

Avoiding the common investing mistake of inadequate research requires a systematic approach to investment analysis, diversifying information sources, and staying up-to-date on market developments. By doing so, investors can make informed decisions, minimize risks, and maximize their chances of achieving their financial goals.

Neglecting Tax Implications

Neglecting tax implications is another common investing mistake that can erode returns and negatively impact an investor’s overall financial strategy. Taxes play a significant role in determining the actual returns on investments, and understanding the tax implications of various investment vehicles can help investors make better decisions and optimize their after-tax returns. In this section, we will discuss why neglecting tax implications is a common mistake and provide some tips on how to avoid it.

Reasons for Neglecting Tax Implications:

- Lack of Awareness: Many investors may not be fully aware of the tax consequences of their investments, leading to suboptimal decision-making.

- Complexity: Tax laws and regulations can be complex and may change frequently, making it challenging for investors to stay informed.

- Short-term Focus: Some investors may prioritize immediate gains over long-term after-tax returns, resulting in higher tax liabilities.

How to Avoid Neglecting Tax Implications:

- Educate Yourself: Gain a basic understanding of the tax laws and regulations that apply to your investments. This may include learning about capital gains tax, dividend tax, and tax-advantaged investment accounts (e.g., TFSA, 401(k), IRA, or Roth IRA).

- Consult a Tax Professional: Seek advice from a tax professional, such as a Certified Public Accountant (CPA) or tax attorney, who can help you understand the tax implications of your investments and develop a tax-efficient investment strategy.

- Consider Tax-Efficient Investment Vehicles: Choose investment vehicles that minimize your tax liabilities, such as tax-exempt municipal bonds, tax-managed mutual funds, or exchange-traded funds (ETFs) with low turnover rates.

- Utilize Tax-Advantaged Accounts: Maximize contributions to tax-advantaged accounts, such as TFSA, RRSP, 401(k)s, IRAs, or Roth IRAs, depending where you reside.

- Manage Capital Gains and Losses: Be strategic about when you buy and sell investments to manage your capital gains and losses. Consider holding investments for more than a year to qualify for lower long-term capital gains tax rates, and use tax-loss harvesting strategies to offset gains with losses.

- Rebalance Tax-Efficiently: When rebalancing your portfolio, consider doing so within tax-advantaged accounts to minimize taxable events.

- Stay Informed: Regularly review tax laws and regulations to stay updated on any changes that may affect your investment strategy.

In conclusion, neglecting tax implications can be a costly investing mistake. By educating yourself on tax laws, seeking professional advice, and utilizing tax-efficient investment vehicles and strategies, you can optimize your after-tax returns and better achieve your financial goals.

Final Thoughts on Common Investing Mistakes to Avoid

Navigating the world of investing can be challenging, but being aware of common investing mistakes can significantly improve your chances of success. By conducting thorough research, understanding the tax implications of your investments, and adopting a disciplined and informed approach to investing, you can minimize risks, optimize returns, and work towards achieving your financial goals.

Remember, investing is a lifelong journey, and learning from mistakes is an essential part of growth. Continuously educating yourself and staying up-to-date with market developments will not only help you avoid these common pitfalls but also enable you to make informed decisions that align with your long-term objectives.

About The Author

Neha Singla (CSC, CPH) is an associate financial planner in Niagara Falls, Ontario Canada. She has millions of dollars under management, and helps her clients plan their finances, investments, taxes, and retirement.